The Federal Government doesn’t want to lift your super from 9.5% a year, despite MPs and Senators getting 15.4%. The more the whole super pool grows, the harder it is to cover up the fact that super funds run by banks and financial institutions – many of them major LNP donors – have been fleecing the public’s super on an industrial scale for decades. This is the story Westpac and News Corporation Australia didn’t want you to see in mid-2018. And they succeeded, even in the middle of a royal commission into banking illegality…

Appreciate our quality journalism? Please donate here

EXCLUSIVE

Westpac has gouged more than $8 billion from the life savings of its almost one million superannuation fund members over the past decade, including by operating a complex web of obscure paper companies, many of which generate huge fees despite many performing no real service and having no employees.

The byzantine and extremely opaque structure of Westpac’s super operations has facilitated the bank, through its “funds management” arm BT Financial Group, in charging vast fees, because consumers, and even most financial advisers and analysts, are unable to understand the almost impenetrable structure.

Massive fees and charges are the key reason why, on average, the 950,000 members of Westpac’s Retirement Wrap, holding $62 billion of retirement savings, has seen growth in overall returns over the entire decade to June 30 2017 of roughly half actual market rates.

It’s even well below the risk-free market returns on “cash” investments in that period and only barely above inflation.

Other superannuation “investment options” run by Westpac’s BT – such as Australian shares, international shares and commercial property investment options – have been similarly gouged, with the total adding up to over $8 billion.

That means the almost 1m Westpac super members, all forced to put between 9 per cent and 9.5 per cent of every pay packet into super over the past decade under the nation’s compulsory super system, have earned almost nothing on those investments.

In other words, those Westpac super members are, literally, little better off than if they had put their money under their mattresses over the past decade-plus,, despite the substantial gains in actual markets over that time. And many are even worse off.

At the same time, the “manager” of those funds for most of the decade – Westpac arm BT Investment Management – gouged on fees.

The value of BT Investment Management, by its own admission, grew astronomically.

Bloated on the fees it was gouging from the 950,000 Westpac super accounts, BT Investment Management grew almost ten times faster than the nation’s top 200 listed companies between 2007 and 2017.

Its shareholders – the biggest being Westpac – were delivered a return of over 600 per cent in that time.

In other words, while the 950,000 people whose super was with Westpac’s BT earned almost zero on their money, BT Investment Management and its owners (Westpac) earned returns of over 600 per cent for “managing” that super.

The “managing” overwhelmingly meant stripping money from those 950,000 super funds.

These revelations come as the Federal Government on Friday released publicly the Retirement Income Review, conducted by former senior Treasury Department official Michael Callaghan.

The Federal Government released the review as the nation was reeling from the release on Thursday of an explosive report that found Australian special forces soldiers allegedly committed 39 murders in Afghanistan.

The LNP Coalition has for many years fought against the so-called “industry” funds, which cannot make profits for their owners, such as Westpac, claiming they direct large sums of money to the union movement and engage in impropriety.

However it is the so-called “retail” funds, those run by the banks and other financial institutions – that make “profits” for themselves for “managing” the super of Australian workers and retirees – that have engaged in rampant gouging of super funds.

Many of the banks and financial institutions that have been involve in the most egregious of these super swindles – including Westpac – are among the biggest donors to the Liberal and National Parties, at both the federal and state levels.

Although politicians are paid superannuation contributions of 15.4%, the Federal Government has suggested it will scrap its earlier promises to lift the super contribution cap for the rest of the population above its current 9.5%.

Westpac and BT have gone to great lengths to prevent the details in this story from being made public. They have worked hard to create an appearance that they have significantly cut fees.

“The investigation has uncovered a meticulously designed system which is almost impossible to navigate but which facilitates an enormous transfer of wealth away from the saving public”

— The Klaxon

In mid-2018, amid the banking royal commission, Westpac announced it would cut some of the fees it charged on some BT super and wealth management funds.

However, The Klaxon can reveal those changes related to around just 10 per cent of the funds managed by the group via its BT Financial Group arm.

Those changes do not relate to most of these existing super accounts, which have been dubbed “rivers of gold” by industry insiders because of the enormous wealth they deliver their managers via outrageous fees and charges.

Westpac has bought up and operated many financial advice firms, and has its own BT “financial advisers” direct people into its shoddy BT superannuation products.

Because it does this, Westpac has argued it is not its fault people are being burned – because they “chose” to make the investments.

The Productivity Commission has found retail, or “for-profit” funds, such as Westpac’s behemoth $62bn Retirement Wrap, have delivered returns well below the market rate, even after accounting for all “reported” fees and accounting for any differences in the type of investments they make (such as investing more in conservative assets).

Billions of dollars in super held as “cash” investments by Westpac earn returns of as little as one quarter of market rates, with the bank claiming the reason was such investments were “at call”.

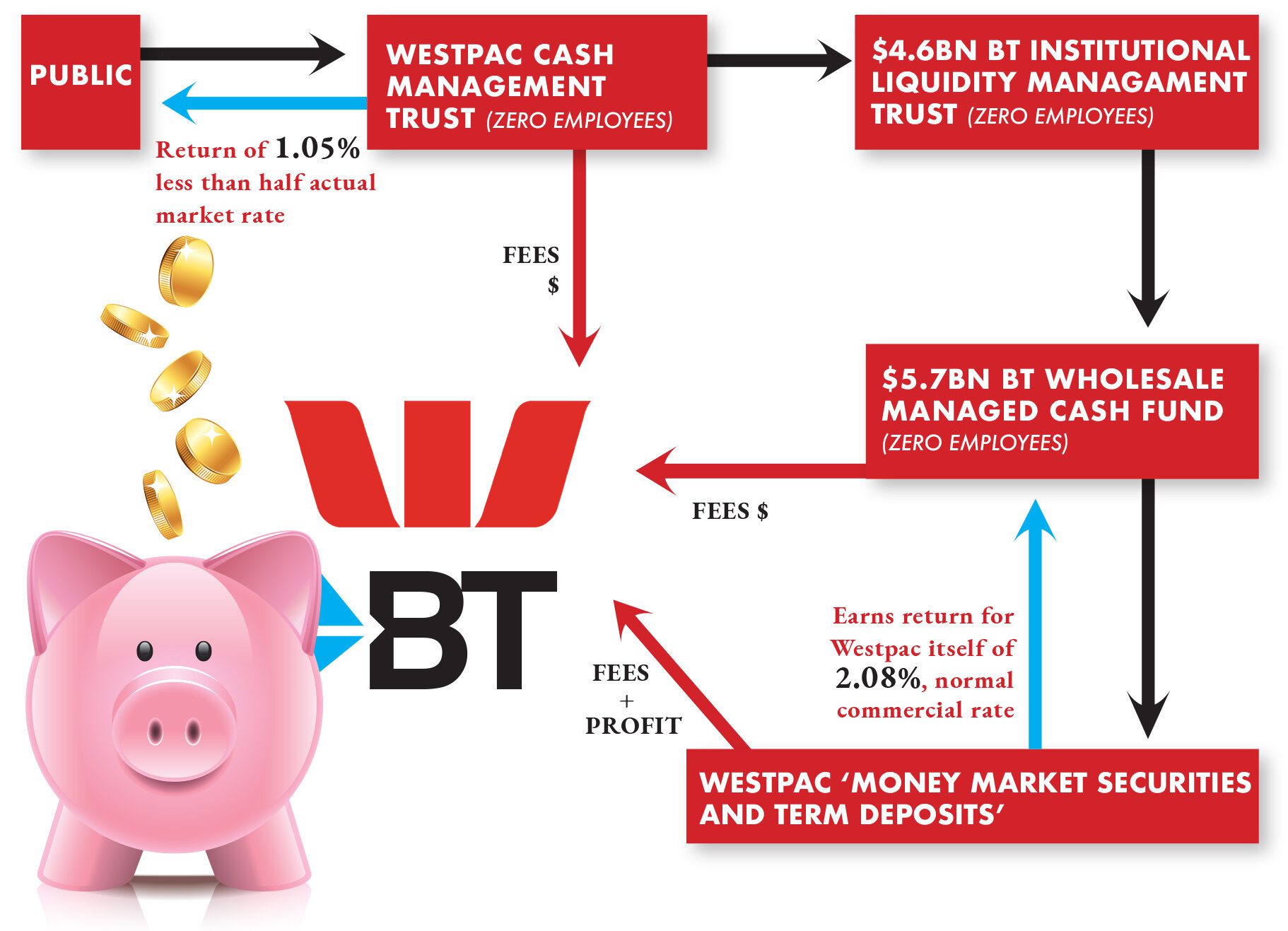

However this investigation shows the vast majority of that money is invested in “money market securities” and “term deposits” — usually Westpac’s — and Westpac is earning actual market rates on that money.

Members of the public, when signing up for super, typically choose from a list of eight or so key options, such as cash, Australian shares or international shares.

For those investors who chose “cash” and were duly placed in Westpac’s Cash Management Trust, Westpac paid them an annual interest rate of 1.05 per cent.

It can now be revealed that that money is moved through two other corporate entities, both of which have zero employees, before Westpac places it in money market securities and term deposits, earning around 2.08 per cent a year, actual market rates. (These figures relate to payments before the recent crash in interest rates).

How Westpac and BT gouges billions from super of workers and retirees. It operates a similar model across almost all investment “options”. Source: The Klaxon, Westpac and BT accounts

Westpac’s BT has engaged in a similar operation of systemic gouging across many of its investment “options” however the fleecing of the “cash” options is easiest to illustrate.

There are other “options” – including cash options – that have been gouged by BT to an even greater extent.

Members of the $62bn BT Retirement Wrap earned average annual returns over the decade to June 30 2017 of just 2.57 per cent a year, which is substantially less than what the money would have earned had it been simply invested in a normal “cash” short-term deposit at a bank.

On the other hand, the fund has delivered billions of dollars to Westpac, funding huge executive bonuses and the bulging pay cheques BT executives receive for “managing” the fund.

The bulk of the money gouged from those super funds has flowed to BT Investment Management, which has long been owned by Westpac, but whose name was changed to Pendal Group in April 2017 after Westpac reduced its holding in the entity.

Fuelled by that money fleeced from super members, the value of the listed Pendal Group rocketed delivering astronomical returns to shareholders — the biggest being Westpac for most of the last decade.

According to BT Investment Management’s 128-page annual report for the year to June 30 2017, the company (called BT Investment Group until two months earlier) delivered total shareholder returns a massive ten times that of its top 200 peers in the ASX 200, the group of the nation’s biggest 200 listed companies.

“Over the past five years, BTIM has produced a total shareholder return of 622 per cent, compared to a 62 per cent increase in the S&P/ASX 200 Accumulation Index, which is testament to the successful execution of our strategy,” the company’s annual report states.

Over just the five years to June 30 2017, BT Investment Manager Emilio Gonzalez earned $27m.

Where the super of almost 1 million Westpac/BT super customers went – to the “shareholders” of BT Investment Management, the biggest being Westpac. BTIM CEO’s salary soared. Source: BTIM

Westpac and BT – including BT general manager of superannuation Melinda Howes – have repeatedly declined to comment on the matter.

In a written statement, Westpac Group Head of media relations David Lording said: “It is wrong and misleading to accuse BT of ‘gouging’ its customers.”

Mr Lording would not confirm whether he “personally” stood by that claim.

Having been presented with detailed analysis of how money flowed through the system – and that investors in the Westpac Cash Management Trust were losing about half their returns in fees (with investors receiving returns of 1.05 per cent, half the market rate) – Westpac said its fees of 0.81 per cent on those funds were disclosed in the trust’s product disclosure statement.

“Over the past five years, BTIM has produced a total shareholder return of 622 per cent…which is testament to the successful execution of our strategy”

— BT Investment Management

That 0.81 per cent fee means Westpac was charging 0.81 per cent a year of every dollar the super member invests in the Westpac Cash Management Trust.

During the period the market rate for “cash” was just above 2%.

The market rate is what the broader investment market is willing to pay in returns for money invested in safe “cash” investments.

Instead of earning the market rate of 2.08% (the rate Westpac was earning on the money) Westpac’s super savers were earning just 1.05%, after Westpac’s gouging.

That means the bank was charging an effective 56 per cent annual fee for “managing” that money, which it simply placed in standard term-deposits or similar.

Even after adding back the extortionate 0.81% fee that Westpac said it had disclosed, there is still money missing.

The money that was returned to super holders (a return of 1.05%) plus the fee (0.81%) equals an annual return of 1.86%.

This is significantly below the 2.08 per cent (market rate) Westpac actually earned on the money at the time, such as by lending it out.

Melinda Howes, head of super at Westpac’s BT, has overseen billions of dollars gouged from super funds. Source: LinkedIn.

Had the hundreds of thousands of investors in the $61bn BT Retirement Wrap instead had their money invested by the federal government’s own sovereign wealth fund – the Future Fund – or the nation’s biggest “industry” funds, such as AustralianSuper, they would be collectively billions of dollars better off.

Our investigation, conducted over hundreds of hours, has involved searching through tens of thousands of pages of documents Westpac and BT have, by law and over many years, filed with corporate regulator the Australian Securities and Investments Commission.

The scores of Westpac/BT “investment options” – such as the Westpac Cash Management Account – exist as “managed investment schemes” in a structure that requires each “scheme” to have a “responsible entity”.

This means each investment option has an associated, audited, set of annual accounts which means it is possible – though painstaking – to track money through the byzantine Westpac/BT network and to see in high detail how the vast gouging actually occurs.

The Klaxon understands this is the first time such analysis has been conducted.

The investigation has uncovered a meticulously designed system which is almost impossible to navigate but which facilitates an enormous transfer of wealth away from the saving public under the nation’s compulsory retirement savings superannuation scheme.

Much of this cost is ultimately borne by all taxpayers by way of an increased dependence on the aged pension by BT superannuation members, many of which are retiring with half the money or less they would have had had they been with a super fund that delivered returns in line with normal market rates.

Major “industry” super funds – close to market returns. Major “retail” funds, barely above inflation. Decade to mid-2017. Source: APRA data

Westpac, which aggressively argued against both the forming of the Financial Services Royal Commission, as well as past government moves to increase protections for super members, has defended its high fees, saying its super members have made the “choice” to invest in the products they have.

In many cases this “choice” had been made by those investors following the recommendations of their financial advisers, who were employed, directly or indirectly, by Westpac and BT.

Under the Superannuation (Supervision) Act 1993 the trustees of super funds – in this case a group of senior executives at Westpac’s BT – are required by law to act in the “best interests” of their super members.

Gouging super accounts to make mega-profits for their own company and its affiliates does not represent acting in the best interests of super investors.

Australia’s superannuation pool is the fourth largest sum of pension money in the world, behind only the US, UK and Japan.

This story was slated to appear in mid-2018 in News Corporation’s The Australian newspaper amid the Financial Services Royal Commission. Westpac and BT senior executives, who were directing large amounts of money to the newspaper at the time, had the story killed after a major behind-the-scenes campaign involving the then editor of the newspaper John Lehmann.